In a globalized economy, what is an “American beer”?

Clearly, if the manufacture, ownership and workforce are all located in the United States, you can select a brand and know you are “buying American.” But in today’s shrinking world, some of these elements may be sited in other countries. Is the resulting beer still American? Is it 50% American? And do consumers care?

Ask a customer what comes to mind when they think of an American beer and the replies, according to retailers, show no consensus.

“If they thought ‘classic American beer,’ typically they would think of Budweiser, Miller, Coors Banquet.” That’s according to Ray Hanning, beer manager at The Fridge Wholesale Liquor in Manhattan, Kansas, naming the traditional flagship beers of the brands that came to dominance in the middle of the last century. All three companies—Anheuser Busch, Miller and Coors—were founded by German immigrants in the mid-1800s. In time, they absorbed or dominated similar German-established companies and became our first truly national brands

Consolidation Brings Changes

In just the past fifteen years, the industry has seen a series of huge shake-ups.

In just the past fifteen years, the industry has seen a series of huge shake-ups.

First, Miller Brewing Company, owned for over three decades by Philip Morris, was purchased by South African Breweries (SAB) in 2002, the first purchase of an American legacy brewery by a foreign company. The new company became SAB Miller.

Three years later, Coors Brewing Company and Canada’s Molson Brewery merged to establish Molson Coors. In 2007, a joint venture brought SABMiller and Molson Coors together to form MillerCoors in the U.S. market.

In 2008, InBev, a Belgian/Brazilian company, acquired Anheuser-Busch to create Anheuser-Busch InBev, the largest brewing company in the world.

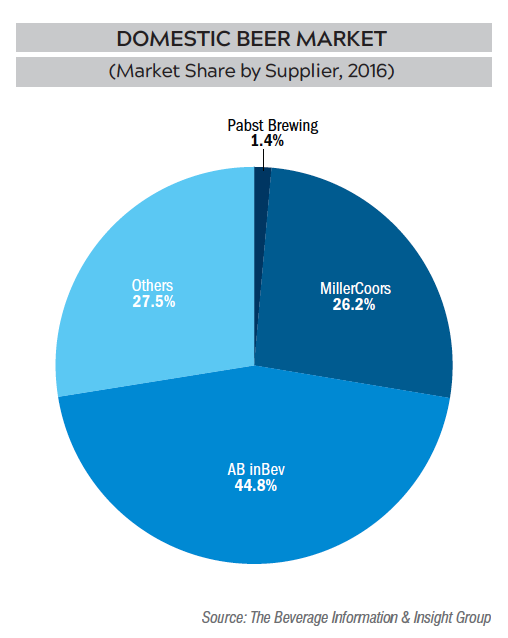

Finally, last summer saw the merger between A-B InBev and SABMiller. The new mega company was compelled to dispose of its MillerCoors brands in the United States, which came under the ownership of Molson Coors. This means that the Big Two— A-B InBev and MillerCoors—still dominate retail shelves in this country.

So, is that an American beer you’re drinking, or a Belgian-Brazilian-Canadian-South African beer?

The fact is, a beer like Budweiser will always be regarded domestically and most places abroad as American—American by history and character—just as Guinness will always be regarded as Irish, despite being owned by London-based Diageo.

“Ownership makes no difference. I don’t see it here,” Hanning says. The list of leading domestic beers from 2014-2016 bears this out (data from Beverage Information and Insights Group). Of the top 25 top-selling beers, 22 are produced by A-B InBev or MillerCoors. Number 11, Yuengling, is the highest-ranked beer from an American-owned company (and the oldest operating brewing company in the country, founded in 1829). Boston Lager, also American-owned, ranks 18th.

If U.S. ownership is an advantage, these two companies don’t play up the fact. “I don’t see that as a big huge aspect of marketing,” says Danny Brager, senior vice president of beverage alcohol practice at Nielsen. “If you look at some of the trends, there are certain beers from other countries that are doing quite well. If [American ownership] was the utmost thing in the minds of consumers, that wouldn’t seem to translate to beers from other countries doing so well.”

And if international ownership is a disadvantage, the attitude seems to be, the less said, the better. For the American brands that are no longer under American ownership, the marketing and iconography has remained resolutely national: briefly last year, Budweiser was even renamed “America.”

Different Clientele, Different Perceptions

Any dismay over the changing ownership of American beer brands has been directed not at what’s been done to the identity of A-B, Miller or Coors, but what’s been done by them to smaller companies.

Hanning recalls only one customer who refused to buy A-B products because of the company’s takeover by InBev: the man had lost his job in St. Louis during the reorganization. Far more customers (admittedly a minority, but vocal) are put off by the purchase of American craft breweries by larger entities.

With the announcement in August that Sapporo had purchased Anchor Brewing Company, a craft pioneer, and Florida’s Funky Buddha would be added to Constellation’s portfolio, at least 17 craft breweries have been acquired by foreign or international brewing or importing companies. It’s hard to keep up.

Brewtopia, a beer and homebrew shop in Keene, NH, caters to an audience that takes these distinctions pretty seriously. When co-founder Zach Cooper asks two customers at the counter to name an American beer, a woman chooses Sam Adams. Her husband cites Battery Steele, a small, newly-opened brewery in Portland, ME.

“It all depends on what level of beer person you’re talking about,” Cooper says. “If you’re talking about your average person who shops at the grocery store, they may say something like Sam Adams or Yuengling. But if you have somebody that is heavily into it, reading the forums, really following craft beer, they are more likely to say a smaller local company, or at least a regional company.”

Rebranding Craft

While sales of classic American lager brands have been flat for many years, the craft sector has enjoyed double-digit growth for a decade or more (though this is showing signs of cooling lately). Large companies have moved into the lucrative American craft territory not only by purchasing craft breweries, but also by brewing their own products in styles associated with craft. The Big Two both have specialty divisions to handle the acquired and in-house craft offerings: The High End (A-B InBev), and 10th and Blake (MillerCoors).

The message is that anyone, anywhere can brew an American craft beer if they are brewing in a craft style.

“The whole idea of people not knowing that Blue Moon is owned by Miller Coors or not knowing that Shock Top is owned by Budweiser – there are definitely consumers out there that don’t know that, thanks to the branding geniuses,” Cooper says.

Realizing that the meaning of the word “craft” was eroding, the Brewers Association (the trade association for American small and independent brewers) recently launched a new voluntary promotional program called the Independent Craft Brewer Seal. Although the certification builds on the BA definition of an American craft brewer (“small, independent, traditional”), the emphasis is on transparency regarding the ownership of the brewery.

The response from The High End was a video with comments from brewers at the craft companies purchased by A-B InBev. Some are sorrowful pleas for beer unity in the face of competition from wine and spirits; others are defiant—and accurate—assertions that the seal is no guarantee of quality.

High End president Felipe Szpigel sums up the essential argument: “And now comes this piece on, you know, independence, and for me the real thinking behind independence is that consumers don’t necessarily care about independence. What they care about is, what is the impact that small businesses have on the communities. And are the communities being better?”

In other words, do consumers care who makes their beer—American or foreign, large or small—and is origin important if the flavor and the cost are attractive?

At Garfield’s Beverage Warehouse outside Chicago, chief buying officer Jeremy Brock sees common trends across all beverage alcohol that “ownership” per se is less important than independence and local qualities.

“You’re seeing that all across the market. Not just with beer, but with liquor, too,” he says.

A recent Nielsen Craft Beer Insights Poll asked frequent (but not exclusive) drinkers of craft beer about the qualities that were important in choosing a craft beer to purchase. “Flavor” and “freshness” topped the list, with 97% and 93% respectively. However, 60% named “locally made” and 55% mentioned “made by an independent brewer.”

“If you look at the marketplace,” says Nielsen’s Brager, “especially in the craft segment where growth is even better, some of the beers that have gone from a local market and expanded nationally, that brings some inherent difficulties. They’re not as well-known in other regions. So there’s almost a bifurcation in the marketplace, where the small and local is performing better from a growth standpoint than the very big craft beers.”

Cooper at Brewtopia sees clear distinctions being made between larger and smaller craft companies. The larger companies, whether or not they remain independently owned, expand distribution and penetration, and change packaging to promote volume sales.

“Once a beer has moved over into your grocery store realm, the sales for a specialty store like ours drop off almost completely,” he says. “If you take a look at Lagunitas, for instance, we went from selling seven different SKUs of Lagunitas down to three. Just this month, we’ve sold 100 fewer cases of Ballast Point than we did last year at the same time.”

“Ballast Point never had a mass-marketed 12-pack until they were purchased, and now they’re about to release one in a price point that is grocery store-specific, something that matches perhaps Sam Adams, or at least the Lagunitas 12-packs, or 21st Amendment, Stone, whoever,” Cooper continues. “But what they don’t understand is that they are also cheapening their brand with the craft consumer by doing that.”

Store Layout Tells a Story

The retailer, the customer and the distributor all influence how beer is shelved, and the final arrangement says a lot about how we perceive and categorize the world of beer.

“Macro imports—Modelo, Heineken, Corona, Stella—they’re all put together,” says Brock at Garfield’s Beverage. “Then all the domestics are together, then we have some macro craft—Goose Island, Sam Adams, Lagunitas, and Founders, now—and then everything else. Big imports, little imports. Local has been very big too. Just like locally grown organic food. It’s kind of what millennials are going for.”

At The Fridge, Hanning has cooler doors devoted to malt beverages and mass domestics. “You have your sweets—your Smirnoff, your Mike’s—and those are going to be the same people who buy the domestics—the Budweiser, Bud Light, Miller Lite, Keystone,” he says.

The rest are organized by place of origin. “The other half of the cooler starts out with what we would consider domestic craft. Being as we have a military installation so close to us, and we have students that come from all over the United States, we regionalize everything,” he says. “So, your first two doors are from Colorado, the next door is from Texas with a little bit of Oklahama in it. The next door is all Kansas, and so on and so forth. If somebody comes in and they ask for Deschutes, then I know they’re a West Coast fan.”

The pattern that emerges is that well-known, big American brands are perceived as domestic, no matter what the global ownership structure. At the other end, the appeal of local products means that consumers for whom that is important are almost always supporting independently owned companies, whether they know it or not.

Under this bifurcation, so-called “big craft” includes Sam Adams, Sierra Nevada and New Belgium – brands that have gone national and seem to have sacrificed some of their excitement to greater volume and reach. Most consumers do not seem to distinguish these independent brands from the likes of Goose Island or Lagunitas (both owned by global companies), or from Blue Moon and Shock Top (both produced by those global companies).

For Nielsen, Brager says, “I try to differentiate between industry definitions versus how consumers think. Industry tries to get really specific as to what’s craft, what’s small, what’s large, what’s regional, what’s domestic. Consumers think a lot more simplistically. Within the industry, people assume that everybody’s super-knowledgeable about every kind of beer or wine or liquor they drink, and that’s not the reality.”

Julie Johnson was for many years the co-owner and editor of All About Beer Magazine. She has been writing about craft beer for over twenty years. She lives in North Carolina, where she was instrumental in the Pop the Cap campaign that modernized the state’s beer laws. Read her recent piece: What’s Behind the Rise of Heavy Beers.